our service

INTERNAL AUDITING

We focus on three types of clients

EN

In case Pre-IPO there are two following main steps:

1. Evaluating internal control risk, divided into two parts;

1.1 COSO–ICIF (in accordance with The SEC internal control sufficiency assessment form)

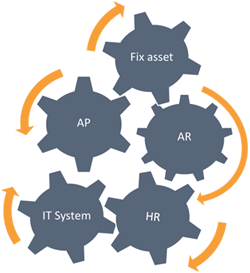

1.2 Evaluate internal control system on each process as follows

Purchasing, sale, payment, safeguard of assets, IT and HR. Including the specific process for some business i.e. production, warehouse, branch offices management, etc.

ENIn case Pre-IPO there are two following main steps:

1. Evaluating internal control risk, divided into two parts

![]()

PLANNING

- Kick-off meeting

- Preparation for interviewing

- Document preparation

- Appointment for visiting client units

![]()

EVALUATING

- Interviewing users

- Reviewing related documents and policies

- Performing the walkthrough

- Drafting IC Checklist

- Evaluating IC

- Discuss result with User

![]()

DRAFTING REPORT

- Supervisory review

- Drafting report

- Sending draft report to client

- Arranging an appointment for the closing meeting

![]()

CLOSING MEETING

- Presenting report for senior management and executives

- Discussing the results of report

- Summarizing result

- Conducting final report

Pre-IPO or Listed company. there are two following main steps:

2. Auditing internal control system (Assurance services)

2.1 Entirely performing substantive testing.

2.2 Following up the remaining risks.

![]()

PLANNING

- Submitting list of documents for auditing in advance

- Kick-off meeting

- Preparation for interviewing

- Document preparation

- Appointment for visiting client units

![]()

SUBSTANTIVE-TESTING

- Interviewing users

- Reviewing related documents and policies

- Performing the walkthrough

- Performing substantive test for fact finding

- Collecting sufficient appropriate audit evidence

- Conducting working paper

- Discuss result with User

![]()

DRAFTING REPORT

- Supervisory review

- Drafting report

- Sending draft report to client

- Arranging an appointment for the closing meeting

![]()

CLOSING MEETING

- Presenting report for senior management and executives

- Discussing the results of report

- Summarizing result

- Conducting final report